Most Australians buy their first investment property the same way they bought their home. They look in suburbs they know. They pick properties they would live in. They make decisions based on how a kitchen looks or whether they like the street.

This is one of the most expensive mistakes in property investing. It leads to portfolios filled with emotionally selected assets in suburbs with average fundamentals, underperforming the market by hundreds of thousands of dollars over a 10 to 15 year hold period.

The strategy for buying an investment property is fundamentally different from buying a home. Here is why, and what to do instead.

When you buy a home, emotion is a valid input. You are choosing where to live, raise a family, and build a life. Proximity to friends, the feel of a neighbourhood, the size of a backyard: these are personal, subjective criteria that matter because you are the end user.

When you buy an investment property, the end user is your tenant and the buyer's market 10 to 15 years from now. Your personal preferences are irrelevant. What matters is whether the suburb's fundamentals support above-average capital growth and whether the property will attract consistent rental demand at a yield that services the debt.

This is a financial decision, not a lifestyle decision. The criteria should be driven by data, not by whether you would personally want to live there.

Home: You choose based on commute time, school catchments, proximity to family and friends, lifestyle amenities, and personal familiarity with the area. These are valid criteria for where you live.

Investment: You choose based on population growth rate, income growth, infrastructure pipeline, housing supply constraints, rental vacancy rates, and historical capital growth data. The best investment suburbs are often ones you have never visited and would not personally choose to live in.

In Australia's current market, the strongest growth fundamentals sit in suburbs across Perth, Brisbane, and Adelaide. Many Sydney-based investors miss these opportunities because they default to buying in suburbs they know, which often sit in mature, expensive markets with lower growth potential.

At Handle Properties, we analyse suburbs against 30+ data points before recommending a location. This is not about gut feel. It is about identifying where the data says growth is likely to occur over the next cycle.

Home: You optimise for liveability. Natural light, kitchen quality, outdoor space, number of bedrooms, architectural character. You are choosing a home that suits your daily life.

Investment: You optimise for broad tenant appeal, low maintenance costs, and land value. The ideal investment property is a house (not an apartment) on the largest land component you can afford, in a suburb with strong fundamentals, that appeals to the dominant tenant demographic in that area.

Houses outperform apartments for capital growth because they capture land value appreciation. Land is a scarce, appreciating asset. Buildings are a depreciating asset. Over a 15-year hold period, the difference between a house and an apartment in the same suburb can be 30% to 50% in total capital growth.

This does not mean the property should be neglected or unliveable. It means you are selecting for investment characteristics, not personal taste. A well-maintained 3-bedroom house on 500 square metres of land in a growth suburb will almost always outperform a beautifully renovated apartment in an established, high-price suburb.

Home: You spend as much as you can comfortably afford, because you are maximising lifestyle quality. Overpaying by $50,000 for the right home in the right street is a trade-off most owner-occupiers accept.

Investment: You buy at a price that makes the numbers work. This means calculating rental yield, cash flow after expenses, loan serviceability, and the total cost of holding the property over the intended hold period.

A rough benchmark for investment-grade property in Australia: aim for a gross rental yield of 4% to 5.5% in growth suburbs, with total holding costs (mortgage, rates, insurance, maintenance, management) that you can sustain without financial stress, even if interest rates move or vacancy periods occur.

Overpaying by $50,000 on an investment property is not a lifestyle trade-off. It is $50,000 of dead money plus the opportunity cost of that capital compounding elsewhere.

Home: You renovate to suit your taste. Kitchen upgrades, bathroom remodels, landscaping, extensions. The return on investment is secondary to the improvement in your daily living experience.

Investment: You renovate only when it produces a measurable increase in rental income or property value that exceeds the renovation cost. Cosmetic improvements that increase rent by $30 to $50 per week (fresh paint, new flooring, updated fixtures) are typically worth the investment. Structural renovations and high-end finishes rarely produce a positive return on investment property.

The golden rule for investment property improvement: spend the minimum required to attract quality tenants at market rent. Every dollar spent above that threshold reduces your return.

Home: You hold indefinitely, or until life circumstances change. You do not typically plan your exit when you buy your home.

Investment: You should have a clear investment thesis and exit horizon before you buy. Are you holding for 10 years for capital growth? Are you buying for cash flow in retirement? Are you building a portfolio to leverage into further acquisitions?

Your hold period determines which markets and property types make sense. A 10 to 15 year growth play calls for a different suburb profile than a 5-year value-add flip. Your strategy should be defined before you start looking at properties, not after.

Familiarity bias is the most common driver of underperforming investment portfolios. You know your suburb, you feel comfortable there, so you buy there. But your suburb may not have the fundamentals to deliver above-average growth over the next decade. The best investment suburbs are identified by data, not by personal geography.

Apartments are cheaper, easier to manage, and often in more convenient locations. But they consistently underperform houses for capital growth because they do not capture land value appreciation. Strata levies, body corporate restrictions, and oversupply risk in apartment-dense suburbs add further downside.

Spending $80,000 on a kitchen renovation that adds $20 per week in rent is a negative return investment. It might feel good if it were your home. In an investment property, it destroys value.

Capital growth is the primary wealth builder, but you need to be able to hold the property long enough to capture it. If your holding costs are so high that you are financially stressed, you risk selling at the wrong time. Model your cash flow conservatively, including scenarios where interest rates rise or vacancy occurs.

The biggest mistake is treating property investment as a one-off transaction rather than a portfolio strategy. Each property you buy should fit a broader plan: target allocation across markets, target portfolio value at a specific time horizon, and a clear understanding of how each asset contributes to that goal.

The investors who build significant wealth through property share a few common practices.

They separate emotion from analysis. They use data to select suburbs and properties, not personal preference. They treat every purchase as a financial decision with measurable inputs and outputs.

They buy houses, not apartments. They prioritise land value and capital growth over convenience or yield. They understand that the land component is the appreciating asset and they allocate capital accordingly.

They think in decades, not years. Property is a long-hold asset class. The power of compounding capital growth over 15 to 20 years is what builds wealth. Short-term thinking leads to buying and selling at the wrong times and eroding returns through transaction costs.

They get professional advice. They use a buyers agent who applies a consistent, data-driven methodology to suburb selection and property sourcing. They use a mortgage broker who understands investment lending structures. They use an accountant who specialises in property tax strategy.

They build a portfolio, not a collection. Each property is selected to serve a specific role in a broader portfolio strategy: growth, yield, geographic diversification, or a combination.

Should I buy an investment property before buying a home? It depends on your financial situation and priorities. Some investors adopt a rentvesting strategy: renting where they want to live while investing where the data says growth will be strongest. This can be an effective way to enter the property market in a high-growth location without being constrained by lifestyle preferences.

Is it better to invest in houses or apartments? Houses consistently outperform apartments for long-term capital growth in Australia because they capture land value appreciation. Apartments can offer higher rental yields in some locations but carry risks including strata costs, oversupply, and limited land value. For most investors focused on wealth building, houses are the stronger asset class.

How many investment properties do I need to retire? This depends on your target retirement income, the value and equity of your properties, and your debt position. A common benchmark is that a portfolio of 3 to 5 well-selected investment properties, held for 15 to 20 years with strong capital growth, can provide a meaningful retirement income through equity or rental income. The key variable is the quality of the assets, not the quantity.

Can I use equity in my home to buy an investment property? Yes. Many investors use the equity they have built in their owner-occupied home as a deposit for their first investment property. This is one of the most common and efficient ways to start building a property portfolio. Speak to a mortgage broker who understands investment lending to understand your borrowing capacity.

What is the minimum deposit for an investment property in Australia? Most lenders require a 10% to 20% deposit for investment property loans, plus purchasing costs (stamp duty, legal fees, inspections). With a deposit below 20%, you will typically need to pay Lenders Mortgage Insurance. The exact requirements vary by lender and property type.

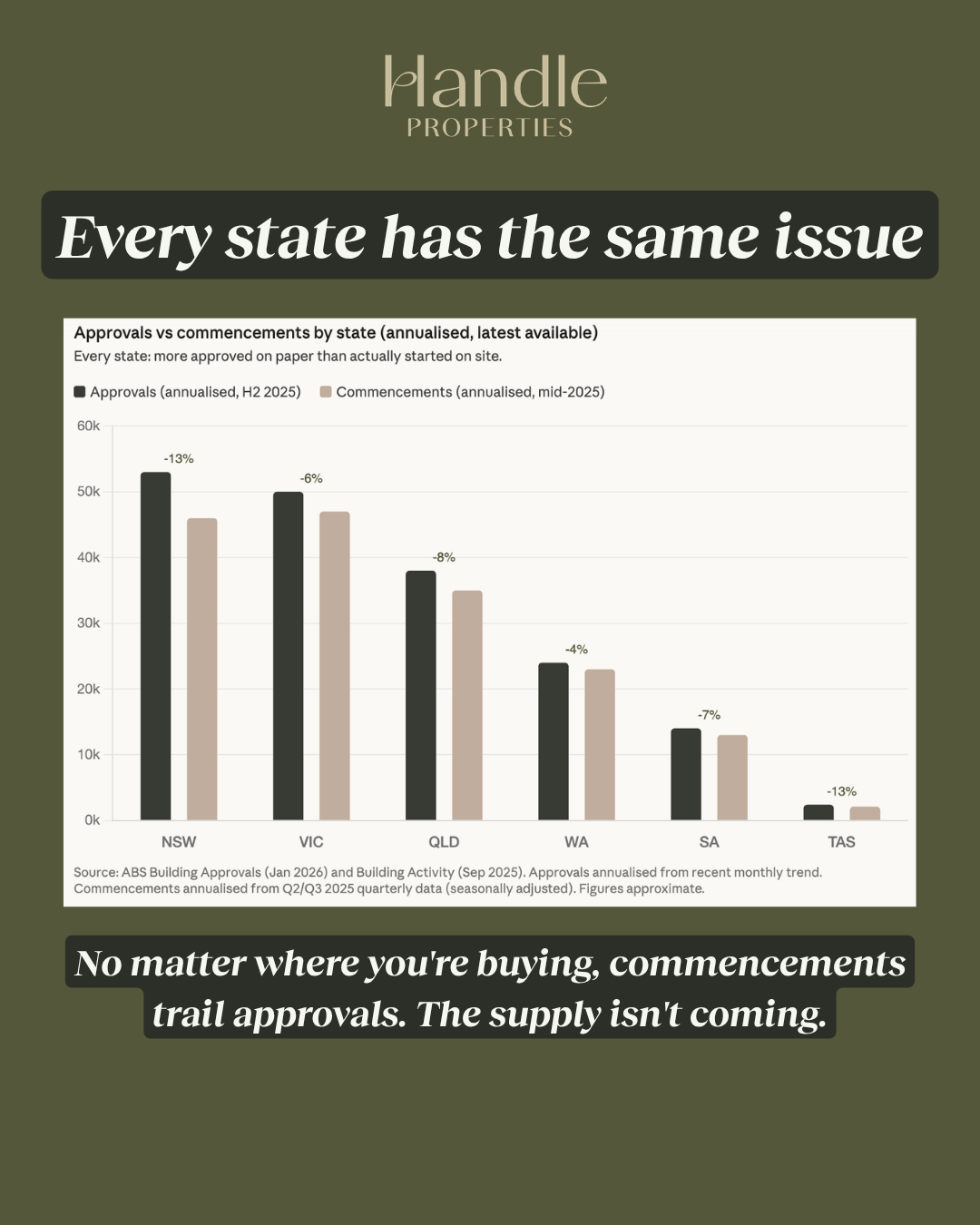

Building costs are surging. Supply is falling. Here's what you should do about it.

View More

Around 20% of Australian property sales happen off-market. Learn how to access these deals, why vendors sell privately, and what gives buyers an edge in this hidden market.

View More.png)

Looking for off-market deals, tired of analysis paralysis, or just don’t have time for the legwork? Book a Call!