Clients have been calling me worried about the May 2026 Budget changes to negative gearing.

I get it. It feels like a big deal. The headlines aren't helping.

So I did what I usually do when something this significant lands. I went and pulled the actual data from the last time the government tried this, in 1985. I wanted to see what really happened, not what the property industry says happened.

Here's the short version: investors didn't leave the market. They adapted. And inside two years, the rules were reversed and prices ran hard.

That's the story most people don't tell.

+42%

More money lent to property investors during the period the rules were changed.

26 months

How long the change lasted before the government backed down.

+24.7%

How much Adelaide house prices jumped in 1988, the year after the change was reversed.

The 1985 timeline, in plain English

How it actually played out.

July 1985

The Hawke government changes the negative gearing rules. Investors can still claim losses against their rental income. They just can't claim them against their

Central Coast Strategic Growth Corridors to Watch

March 22, 2026

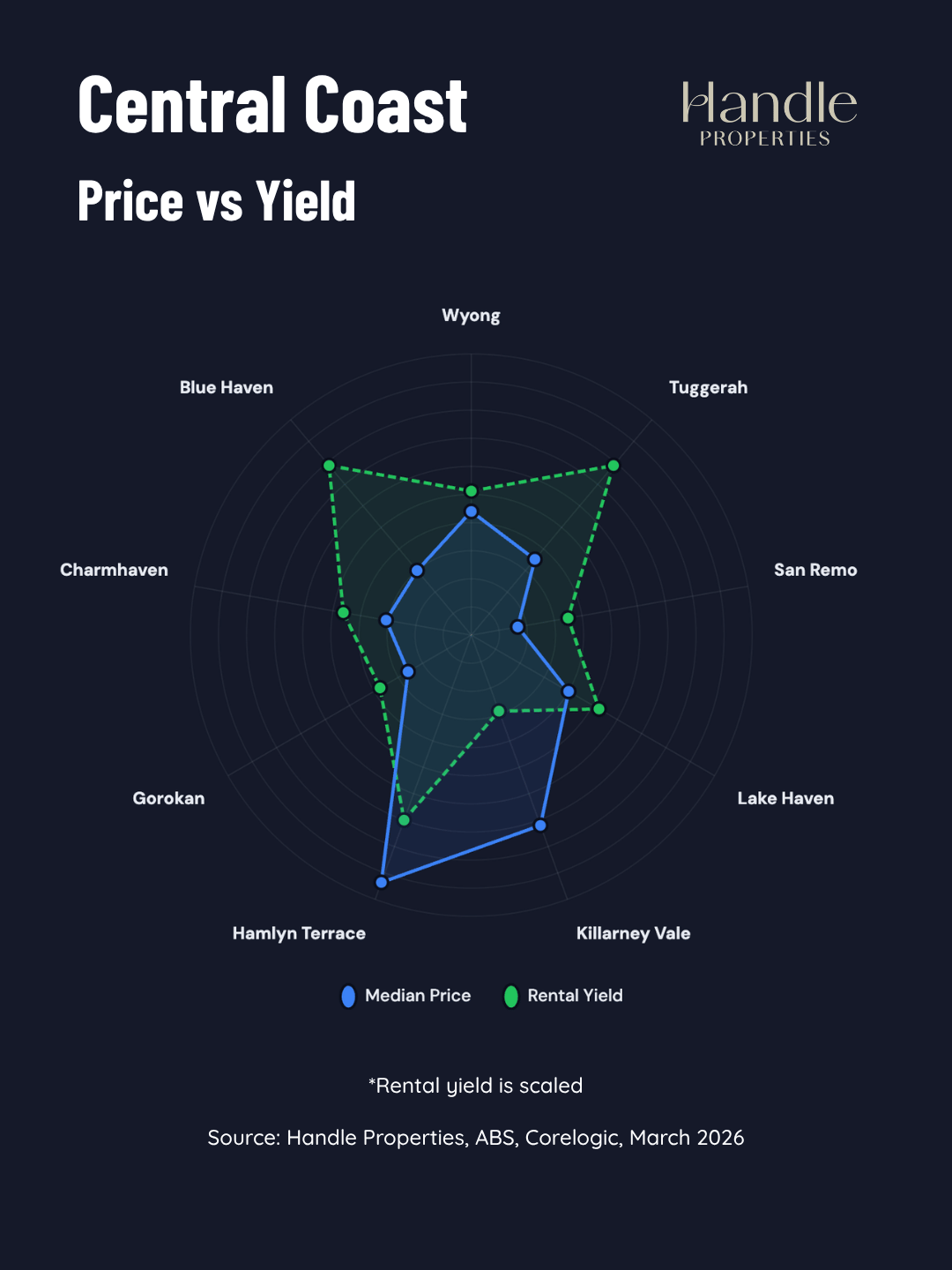

The Central Coast has quietly become one of the strongest corridors for property investors in NSW. Sitting 60 to 90 kilometres north of Sydney, the region benefits from rail connectivity, relative affordability, and sustained population growth across the Central Coast LGA.

We analysed nine suburbs using 30+ data points spanning yield, price momentum, supply dynamics, and tenant demand. Here is how they stack up.

Tuggerah (SA3: Wyong)Yield: 4.03% | Handle Properties Score: 72

Tuggerah punches above its weight with a 4.03% yield and the strongest quarterly momentum in this group at +4.75%. Rail access, proximity to Tuggerah Westfield, and the M1 corridor underpin tenant demand. Low stock on market (0.50%) and fast days on market (20 days) signal tight supply conditions. Annualised growth trajectory points to ~19% if momentum holds, making it the standout mover on the Central Coast right now.

Hamlyn Terrace (SA3: Wyong)Yield: 3.96% | Handle Properties Score: 70

A newer, family-oriented suburb benefiting from modern housing stock and school infrastructure. The 3.96% yield is strong for the price point ($984k median), and quarterly growth of +3.58% reflects rising demand as buyers get priced out of inner Central Coast suburbs. 12-month rent growth of +8.70% confirms tightening rental supply. One to watch as infill continues.

Blue Haven (SA3: Lake Macquarie)Yield: 4.03% | Handle Properties Score: 68

Blue Haven matches Tuggerah on yield at 4.03% but at a lower entry price ($825k). Days on market sit at just 15, the fastest in this group, signalling strong buyer competition. Owner-occupier rates are moderate (67%), leaving room for investor acquisition without skewing the tenant pool. Solid fundamentals for cash flow-first buyers.

Charmhaven (SA3: Wyong)Yield: 3.77% | Handle Properties Score: 66

Positioned between Gorokan and Lake Haven, Charmhaven benefits from affordability ($827k) and steady quarterly growth of +2.73%. Rental demand is stable with low vacancy (0.94% across the LGA corridor). The 5-year median price growth of +56.78% shows this suburb has been quietly compounding. Not flashy, but consistent.

Gorokan (SA3: Wyong)Yield: 3.70% | Handle Properties Score: 65

Gorokan is the volume play in this corridor: 204 average annual sales make it one of the most liquid suburbs on the Central Coast. 12-month price growth of +13.99% is the strongest in this group. At an $815k median, it remains accessible. The trade-off is a lower owner-occupier rate (60%), so watch for rental market saturation in downturns.

San Remo (SA3: Lake Macquarie)Yield: 3.68% | Handle Properties Score: 65

The lowest median price in this group at $792k makes San Remo the entry-level play. Stock on market is razor thin at 0.22%, the tightest supply metric here. Five-year price growth of +64.64% is the strongest across all nine suburbs. Low supply, strong historic growth, affordable entry; classic momentum profile.

Lake Haven (SA3: Wyong)Yield: 3.82% | Handle Properties Score: 64

Lake Haven sits at the commercial heart of the northern lakes corridor with strong retail infrastructure. Zero rental listings at the time of data pull signals extremely tight rental supply. Quarterly growth is modest at +0.59%, but the 5-year growth of +57.41% confirms long-term trajectory. Best suited to buy-and-hold investors targeting reliable cash flow.

Killarney Vale (SA3: Gosford)Yield: 3.63% | Handle Properties Score: 63

The highest volume suburb in this group with 153 average annual sales and a higher price point ($930k). Quarterly and 12-month price growth are soft (+0.54% and +0.95% respectively), suggesting the suburb may be in a consolidation phase after strong prior gains. For investors, this could represent a re-entry window before the next leg up.

Wyong (SA3: Wyong)Yield: 3.81% | Handle Properties Score: 62

Wyong carries the name recognition and rail connectivity, but elevated stock on market (0.98%) and higher days on market (53) suggest the market is softer here relative to peers. Flat quarterly growth (0.00%) reinforces that. The trade-off is that Wyong's town centre revitalisation and proximity to the hospital precinct position it well for medium-term uplift once absorption catches up.

Source: Handle Properties, ABS. General information only. Not financial advice. Past performance is not indicative of future results.

Related Insights

Building costs are surging. Supply is falling. Here's what you should do about it.

View More.png)

Stop Analysing. Start Acquiring.

Looking for off-market deals, tired of analysis paralysis, or just don’t have time for the legwork? Book a Call!